Domains

Internationalised domain names

The registration of internationalised domain names (IDNs) with macron vowels, which feature in the Māori language, an official language under New Zealand law, are allowed in the .nz domain space.

These IDNs are supported in the IRS portal and in the EPP API.

EPP uses the IDN 1.0 EPP extension. This extension must be used when registering IDN domain names. For full details of the extension see : idn-1.0 - RFC Draft: eppext-idnmap

Please see the IDN support in .nz section in this site.

The IRS registrar guide also contains details on using IDNs in the IRS portal and provides EPP examples.

Domain information

Domain information can be retrieved from the registry via the EPP domain info commands and/or using the IRS portal. In addition to the IRS portal query/search functionality.

The IRS portal provides a number of built-in domain name management reports which can be downloaded in CSV format:

Activity Summary — displays a list of all of the interactions with your registry.

Transaction Details — displays a list of financial transactions for a configured reporting period.

Domain Names List — displays a list of all of the domain names for your registrar account.

Domain Fields

Reseller name

“Reseller Name” is a field associated with a domain. The reseller field is an optional string that registrars can use as they like. The intent is for registrars who have resellers to record the reseller name for the domain. The field will not be part of the WHOIS results. The field will be cleared when a domain is transferred between registrars.

The reseller name property is available in the IRS portal or, if using EPP, can be specified in a Domain Create or Domain Update request. EPP requests will require the fury-2.0.xsd extension, the reseller name property is defined using the fury:key RESELLER_NAME.

Domain privacy

In the IRS privacy is set at the domain level.

Please refer to the new .nz policy (section 6) for the policy and operational rules for setting domain privacy (section 6.2. Operational rules). Eligible domain name holders can elect the privacy option at the time of registering a domain name and can change their selection at any time afterwards.

Note

Note: Privacy applies to all contacts associated to a domain including secondary contacts that may be a mix of individuals and organisations.

Domain management

Creating a domain

Domains can be created using the IRS portal or via the EPP API.

Updating a domain

Domains under sponsorship of a registrar can be updated using the IRS portal or via the EPP API.

Renewing a domain

Term In the IRS the registration term is yearly with a range of 1 to 10. This means the minimum registration period is 1 year.

Auto Renew + term

In the IRS all auto-renews will default to the minimum 1-year term.

Any renewal with a term longer than 1-year needs to be done via an explicit renew command.

Deleting a domain

In the IRS domain name cancellations must be done explicitly using either the portal or an EPP delete command.

When a domain is deleted it goes into the redemptionPeriod lifecycle status and the PendingDelete server status and will stay there for ninety days unless it is restored by the registrar.

At the end of the redemptionPeriod, the domain goes into the pendingDelete lifecycle status, and the domain is assigned a Droplist where it will get released when that session is processed. Once the domain has moved to pendingDelete state there is no option to restore it. The period between the end of the redemptionPeriod and the TBR session is currently set to a minimum of 48 hours

There are two situations where a domain is deleted in the IRS and it does not go into TBR:

When a domain is deleted from addPeriod; it does not go into redemptionPeriod, but is immediately released; and

When a domain is deleted that has a Block tag on the Create event, it goes into redemptionPeriod as per normal, but when it reaches the end it does not go into a TBR session, as it is blocked from being re-created, it is immediately released. Note. the Block tag prevents it from being registered again.

For these two scenarios, the pendingDelete period is zero so effectively the domain is released immediately, the next housekeeper run sees that pendingDelete has expired and deletes the domain from the database. IRS housekeepers run roughly every 5 minutes. For these two scenarios, the pendingDelete period is zero so effectively the domain is released immediately, the next housekeeper run sees that pendingDelete has expired and deletes the domain from the database. IRS housekeepers run roughly every 5 minutes.

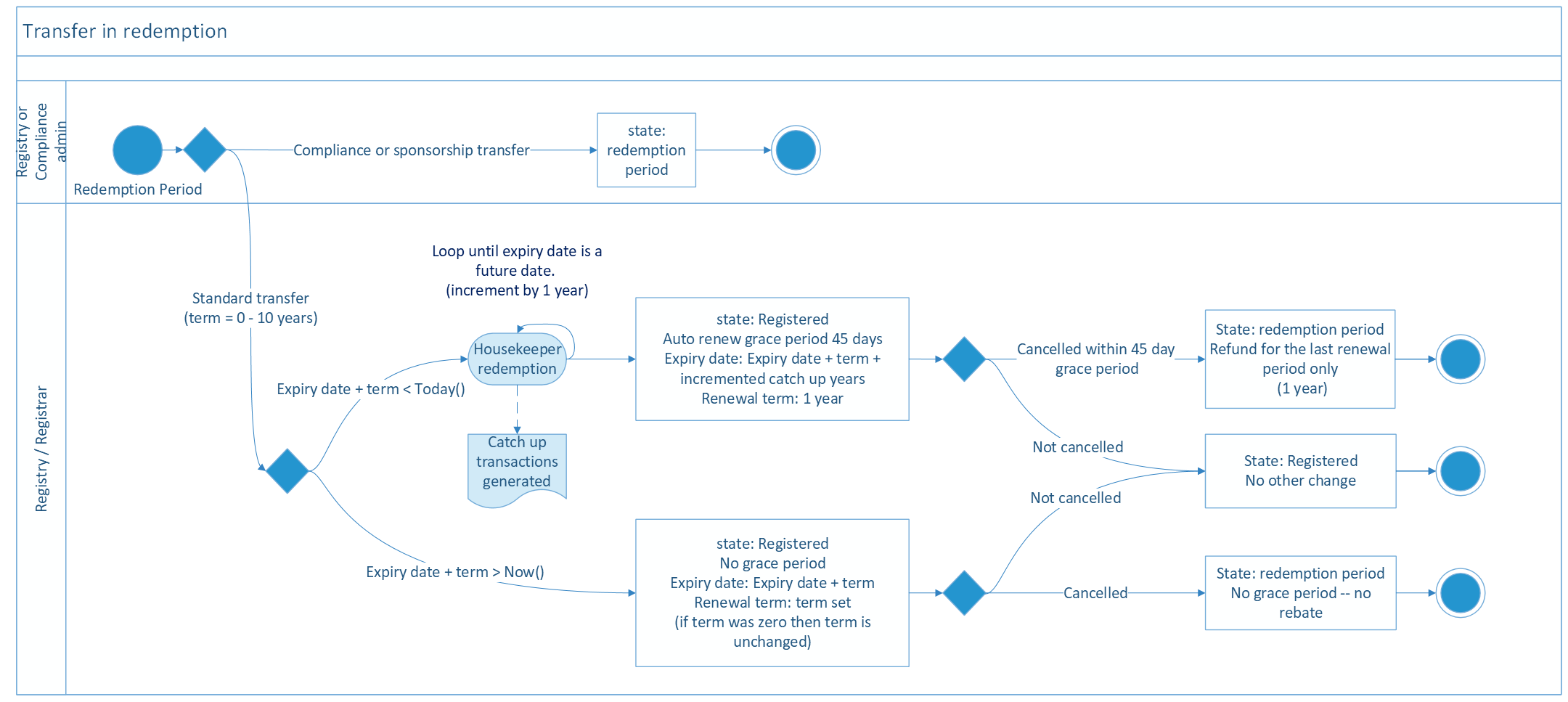

Transferring a domain

If a domain is explicitly renewed by the sponsoring registrar as part of the transfer request, there is no renewal grace period. This means that if the domain is deleted within 5 days after the transfer there will be no rebate for the renewal.

Registrars can transfer a domain that is in redemptionPeriod. A example scenario would be:

the domain holder requests the auth code from the current sponsoring registrar of the domain,

the current sponsoring registrar generates a new auth code,

the current sponsoring registrar provides the auth code to the domain name holder,

the current sponsoring registrar updates the domain with the new auth code value,

the domain name holder provides the auth code to the new sponsoring registrar,

the new sponsoring registrar will complete the transfer and,

the auth code on the domain will be initialised by the system if the transfer was successful.

For domains in the redemption period state on a transfer if no additional term is applied to the domain, a housekeeper job may be triggered to bring the expiry date on the domain up to date. See diagram below.

Restoring a domain

The IRS requires both a restore request and restore report command before restoring a domain name.

The pending restore period, 5 days, is the time allowed between posting a restore request and a restore report. If a restore report is not received then the domain returns to a redemption state.

Registrars can issue a request and a report immediately after each other via EPP, and if using the IRS portal to restore a domain, the commands are grouped, it’s assumed that if a Registrar is going to do a restore request, they’ll want to do the report, so by clicking Restore Domain and entering the information, both are automatically issued simultaneously. They will show up as two separate commands in the history. Typically a restore request and a restore report are processed within the same second so registrars should not see the pending restore status.

Suspending a domain (undelegate)

To suspend a domain name in the IRS so that it is no longer included in the .nz zone file (The domain name will not resolve in the DNS), the clientHold domain status needs to be set. This can be done via EPP or the IRS portal. To include the domain back in the .nz zone file, remove the clientHold status.